Welcome to the April Mutual Fund Observer!

My mom used to say, “March sometimes comes in like a lion.” She never added, “and then it eats you.”

March, named for the God of War, strikes me for two reasons. First, it is the month that has encompassed a whole series of catastrophes in the financial markets and beyond. March 2025 marked:

- The fifth anniversary of the COVID lockdowns and flash crash, in which the S&P 500 lost 34% in 33 days.

- March 24 was the 25th anniversary of the collapse of the dot-com bubble, which vaporized $5 trillion in market value (about the amount vaporized in Q1 2025, but 2020 was back in the days when a trillion still counted for something) and saw the NASDAQ down nearly 80%.

- The 30th anniversary of the social media revolution, sparked by Yahoo! and the Yahooligans.

- The 87th anniversary of Hitler’s Anschluss, the annexation of Austria which marked Nazi Germany’s first act of territorial expansion, violated international treaties, emboldened Hitler’s aggression leading to World War II, and intensified persecution of Austria’s Jewish population under Nazi rule.

- And the 107th anniversary of the outbreak of the deadly Spanish flu epidemic – which infected a third of the world’s population and killed 50 – 100 million – began. (To be clear, they died of influenza or secondary bacterial infections, not from a not-yet-invented flu vaccine or mysterious military vaccine.)

Second, perhaps there’s something to be taken from the fact that we’ve survived so many end-of-the-world catastrophes that we don’t even remember them anymore. We have been exceptional in many ways, and that has served us well for more than a century.

The question becomes, will we choose to remain exceptional in a positive way? If you make the answer based on three months, it is “no.” But we’re not judged on the unusual moments; we are judged by what we choose to embrace – or simply permit – over time. I have faith in us, if only because a vast number of people have committed their lives to making their communities, our nation, our world, and our generation a better place.

Volatile March was named for the god of war. April, in contrast, was named for the eternal turning of the seasons. Its name likely derives from the Latin word for “budding out” or “opening.” Celebrate the unchanging change. There is an uncertain flutter of the seasons here where a warm week is herald to the first spring blooms … which are quickly buried in the last winter snows. And still, they endure the adversity, certain that their day will come.

Celebrate, dear readers, the seasons, the things which change, and the things which never will.

In this month’s Observer …

I am not optimistic about the prospects for the US stock market. That’s not a prediction, dear friends, that’s just a disclosure of a personal perspective. Markets thrive on predictability since investment decisions need to be made in the framework of a three-to-five-year plan. (Speculation, not so much.) Given the proliferation of policy by pique, investors are not likely to have the necessary confidence to make steady and ongoing commitments to the US equity market. Or, they might surprise us. This month and next MFO will try to address some of the angst caused by that instability. In general, long-term investors need to stay in the equity market. That’s far easier if your exposure is hedged. Hedging can be either cheap and easy or complex and expensive. We prefer the former, and so this month, we’ll profile The Dry Powder Gang, 2025. The Dry Powder Gang are outstanding funds that, like Warren Buffett, are willing to sit on cash when equities aren’t paying for the risk you’re taking.

In May, we’ll profile the handful of hedged funds that actually earn their keep.

We share a Launch Alert for GlacierShares Nasdaq Iceland ETF, a fund that will divide its portfolio about evenly between the stocks of Icelandic companies and the stocks of companies in other (primarily) Nordic nations with substantial ties to Iceland. There’s been an upsurge in the ranks of the Arctic-curious, from investment managers to … uh, politicians whose eyes have turned north toward Greenland, Norway, and the Nordic nations generally. The combination of sound economies and healthy national cultures, combined with anxiety about a stretch of unhabitable real estate, has more folks pondering the potential of the North.

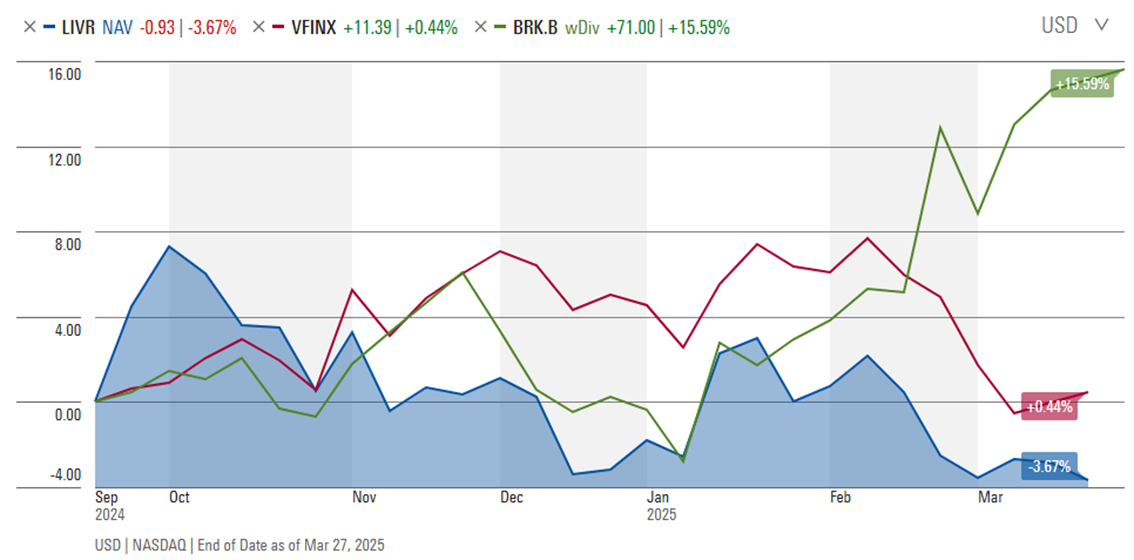

I teach about Communication and Emerging Technologies (cool day job, eh?), and few technologies are more emergent than artificial intelligence. There’s a credible argument that virtually every profession in the world will, within five years, be reshaped by artificial intelligence, and the investment industry is no exception. Morningstar has taken tentative steps toward creating a human-light analytic environment (from its Q-analyst ratings driven by machine-learning technology to its AI spokesmodel, Mo), while a dozen investment managers have committed to AI-driven portfolios. In “The Ghost in the Machine,” I’ll walk you through what AI is, how the AI models running one portfolio – Intelligent Livermore ETF – recommend you treat their fund, and finally, what qualifies as the bigger picture of AI fund management.

I teach about Communication and Emerging Technologies (cool day job, eh?), and few technologies are more emergent than artificial intelligence. There’s a credible argument that virtually every profession in the world will, within five years, be reshaped by artificial intelligence, and the investment industry is no exception. Morningstar has taken tentative steps toward creating a human-light analytic environment (from its Q-analyst ratings driven by machine-learning technology to its AI spokesmodel, Mo), while a dozen investment managers have committed to AI-driven portfolios. In “The Ghost in the Machine,” I’ll walk you through what AI is, how the AI models running one portfolio – Intelligent Livermore ETF – recommend you treat their fund, and finally, what qualifies as the bigger picture of AI fund management.

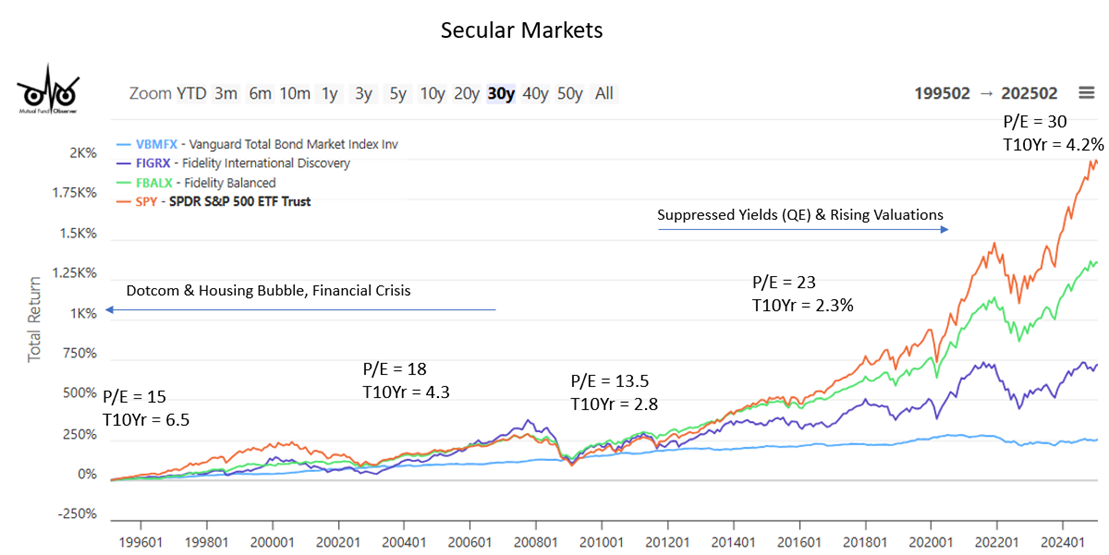

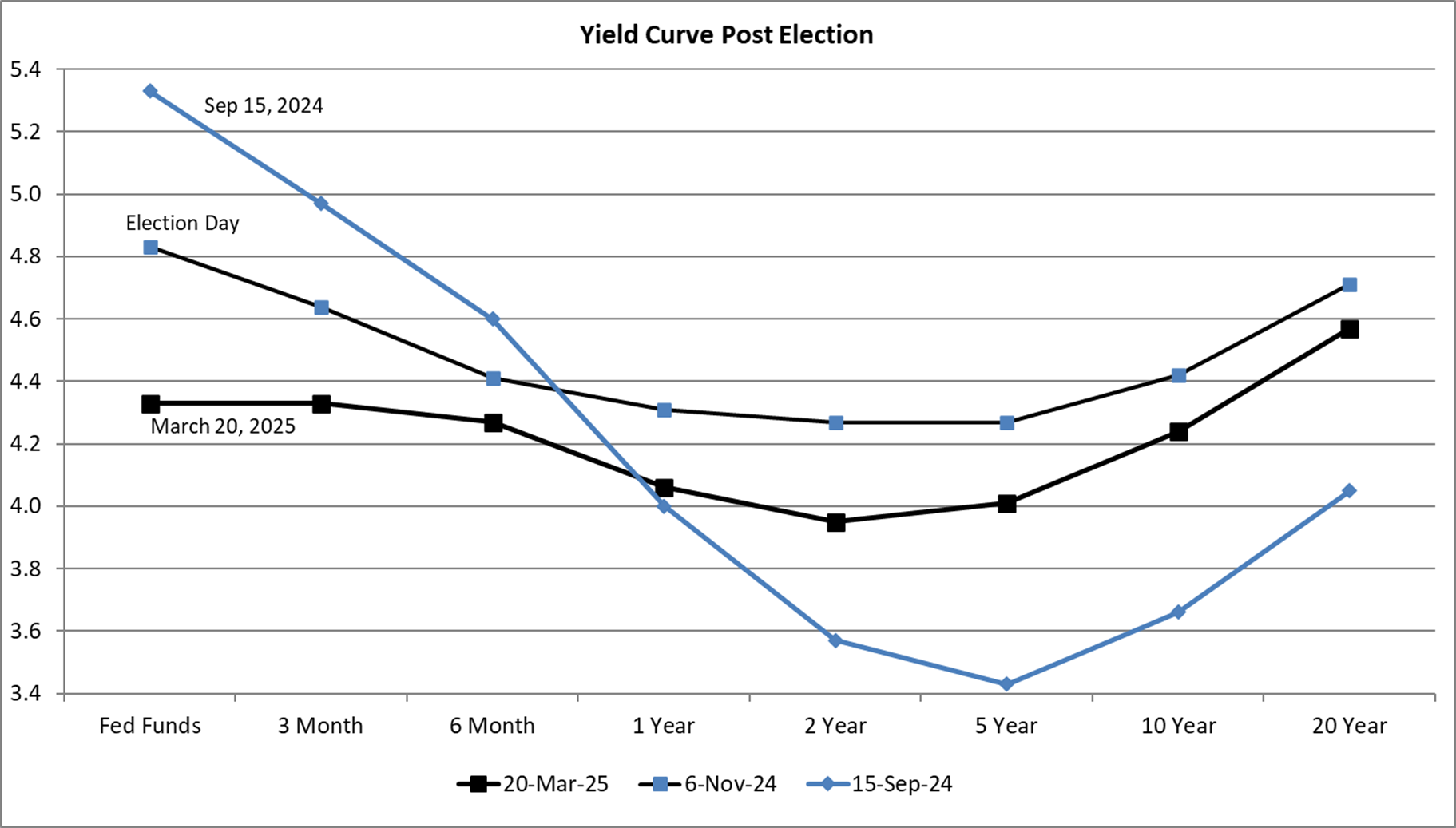

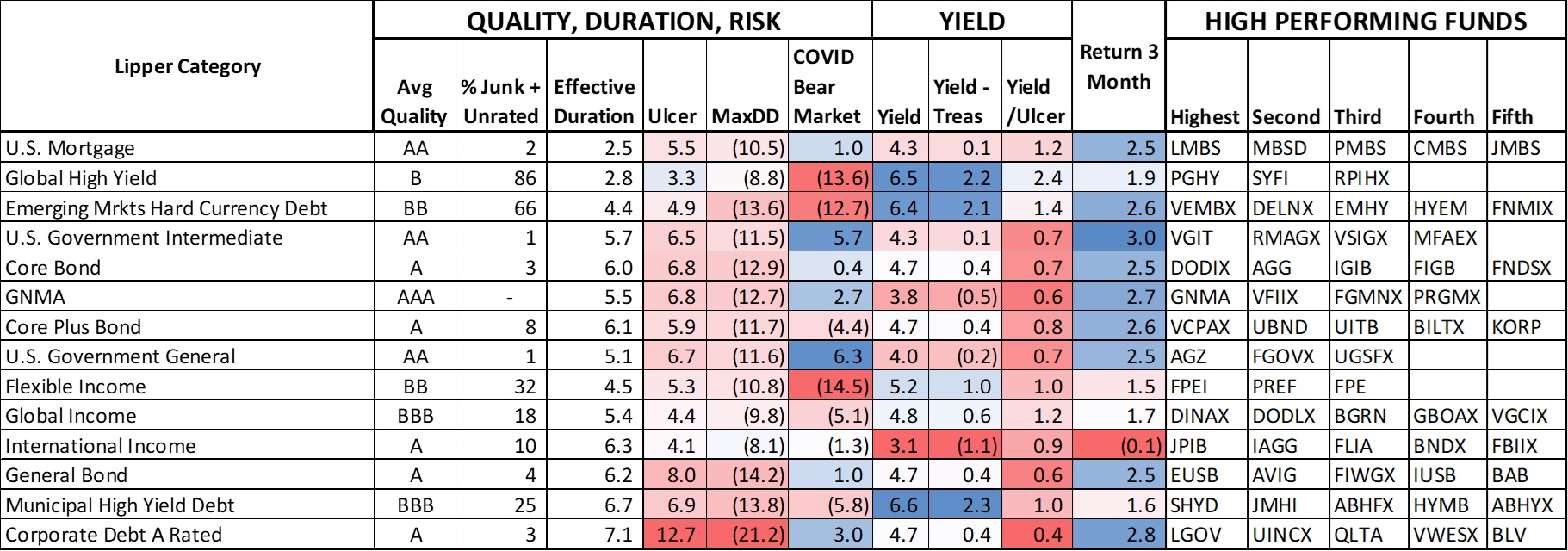

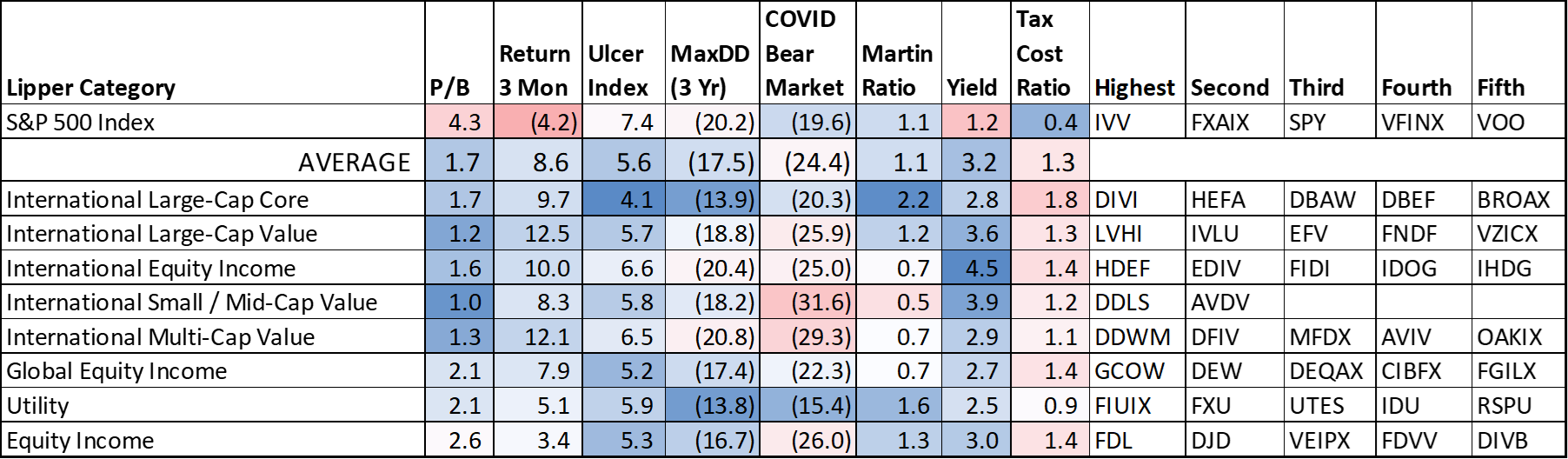

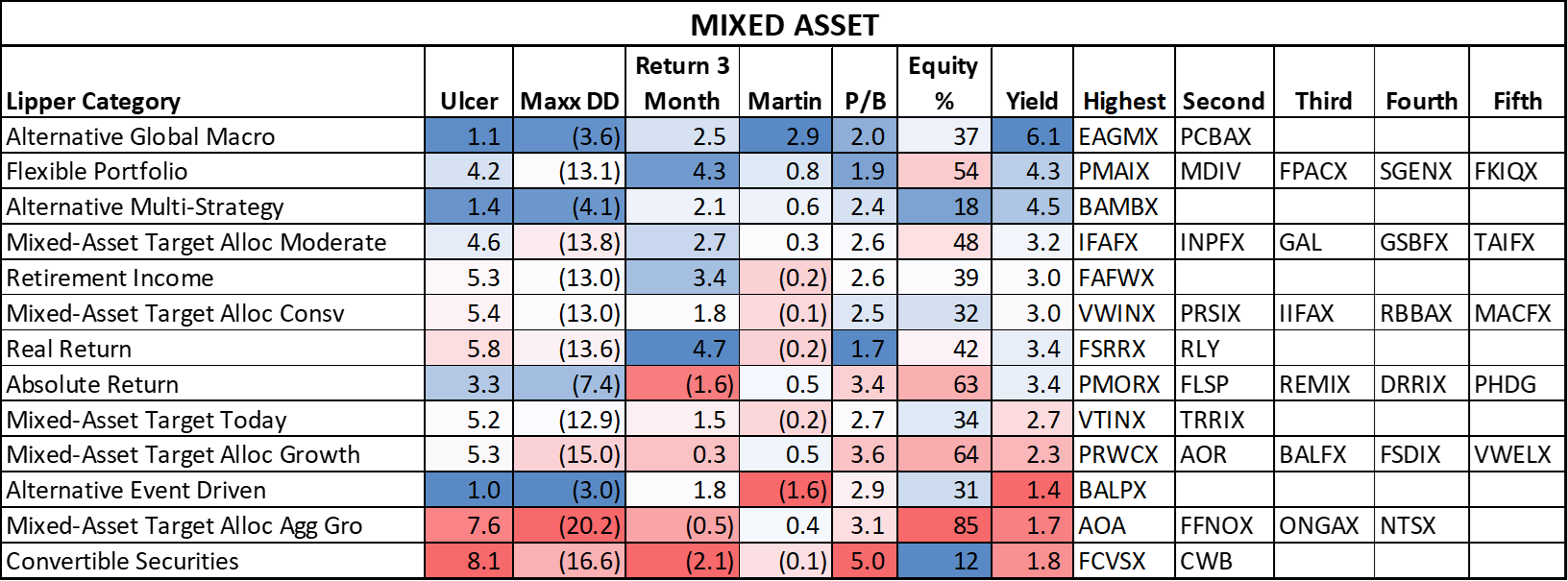

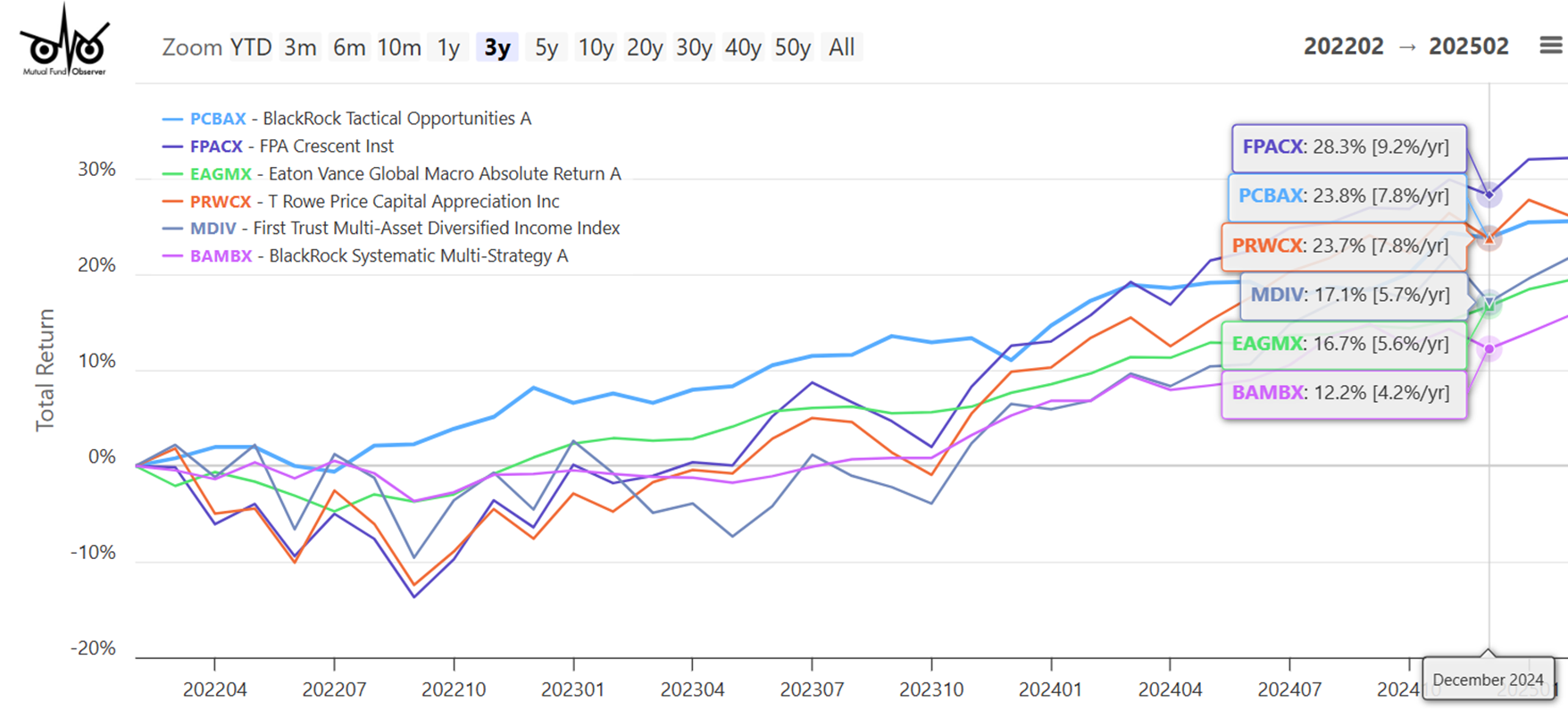

Lynn helps us all get grounded again. His April articles continue the theme he’s been developing all year, highlighting how bonds provide stability and income while international equities offer better valuations than U.S. stocks. In Overview of Secular Markets Lynn Bolin examines long-term market trends, contrasting the 1995-2012 period with recent years. He notes that elevated P/E ratios and changing economic conditions suggest international equities and bonds may outperform U.S. stocks in coming years. Bolin analyzes current treasury yields, bond returns, and mixed-asset funds, recommending a diversified portfolio given current market uncertainty.

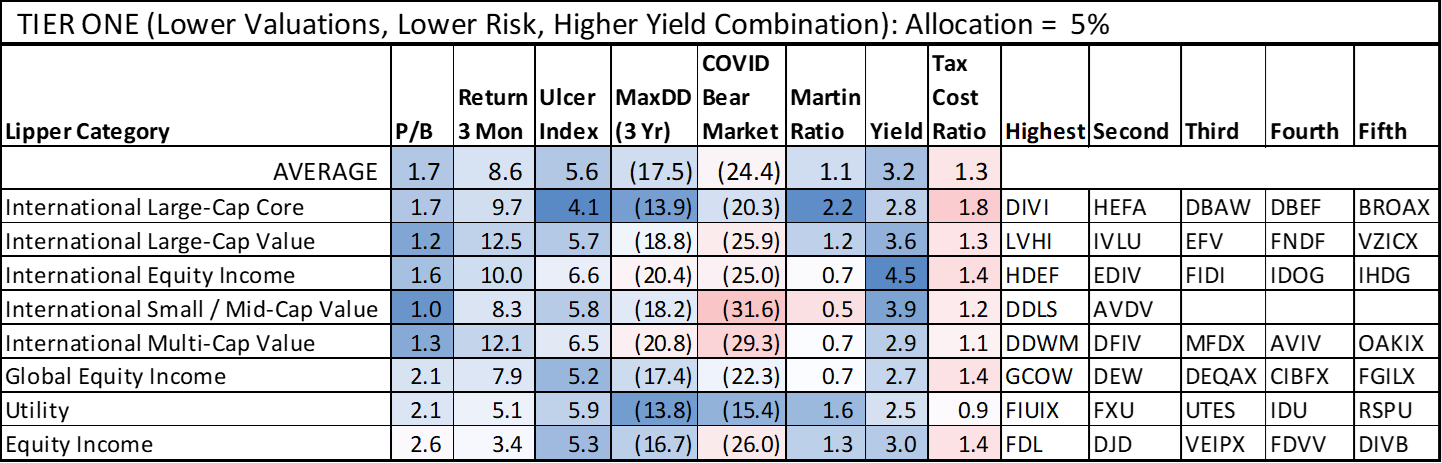

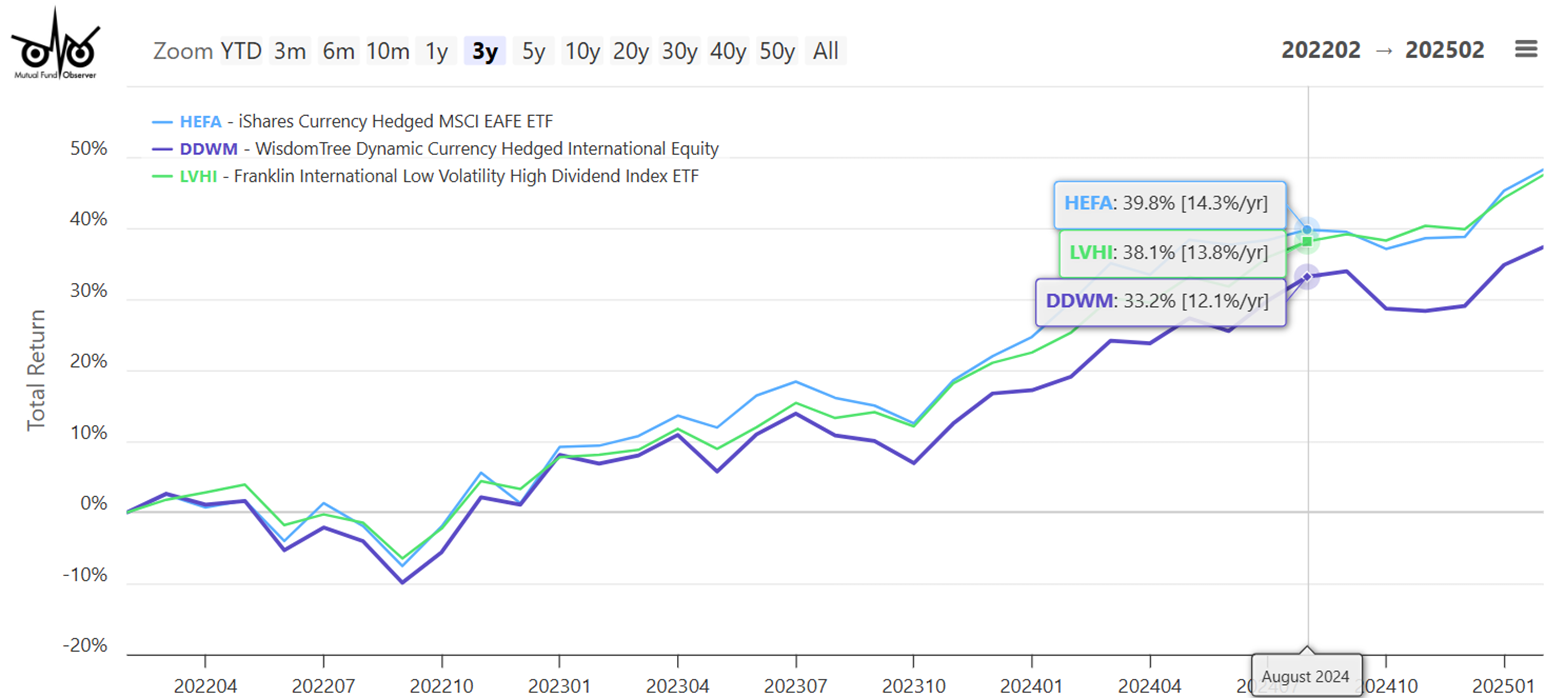

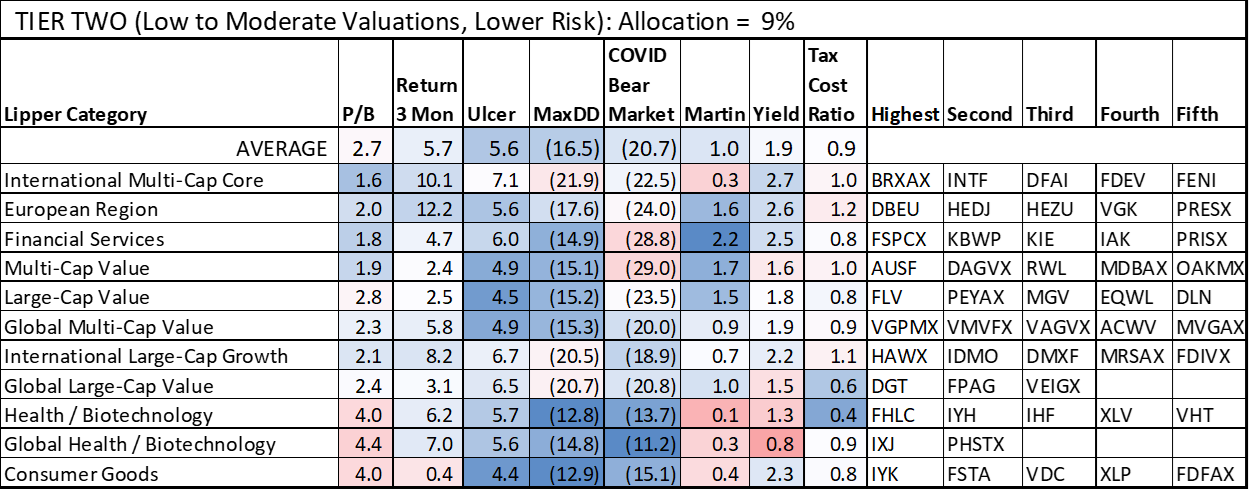

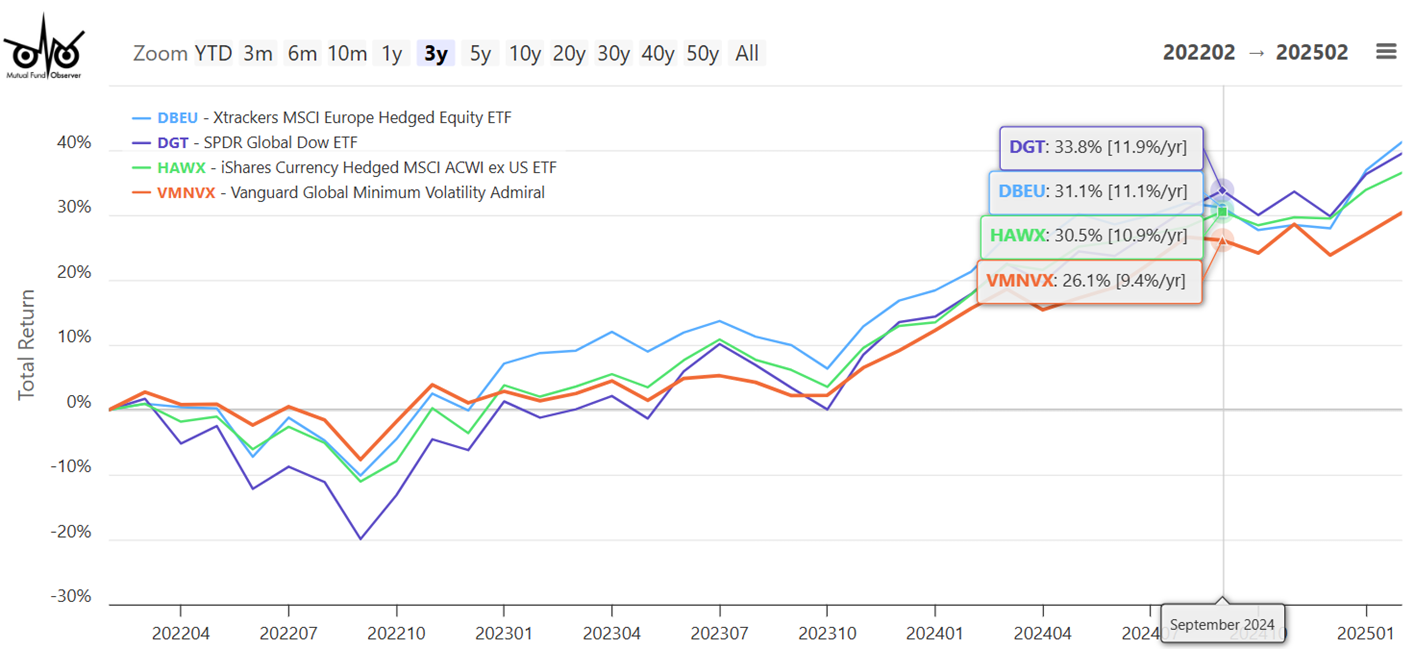

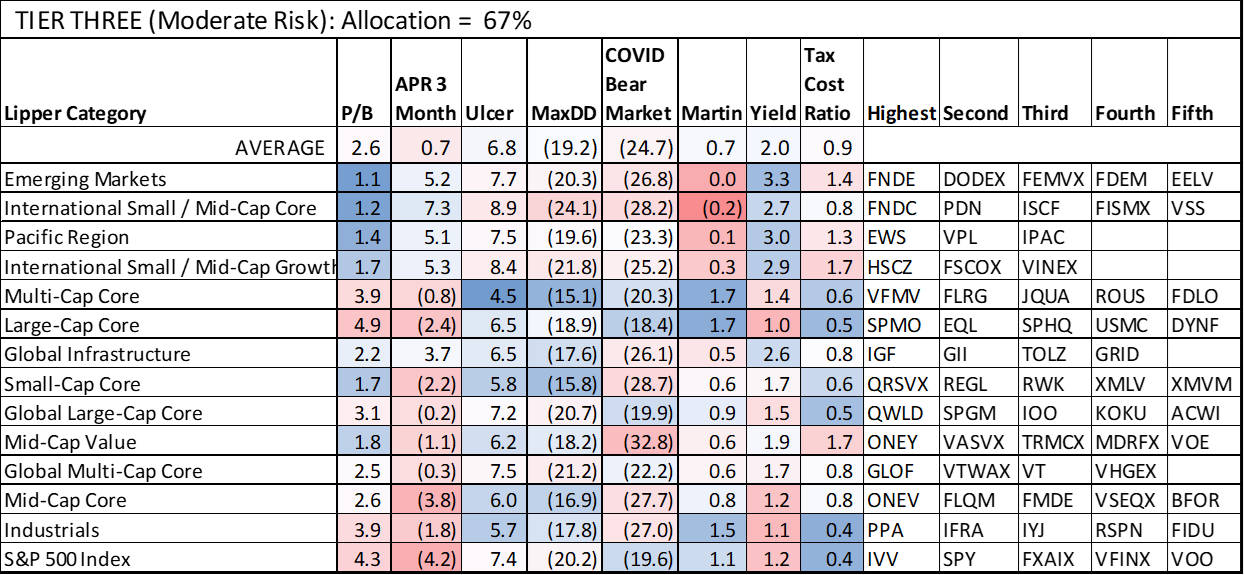

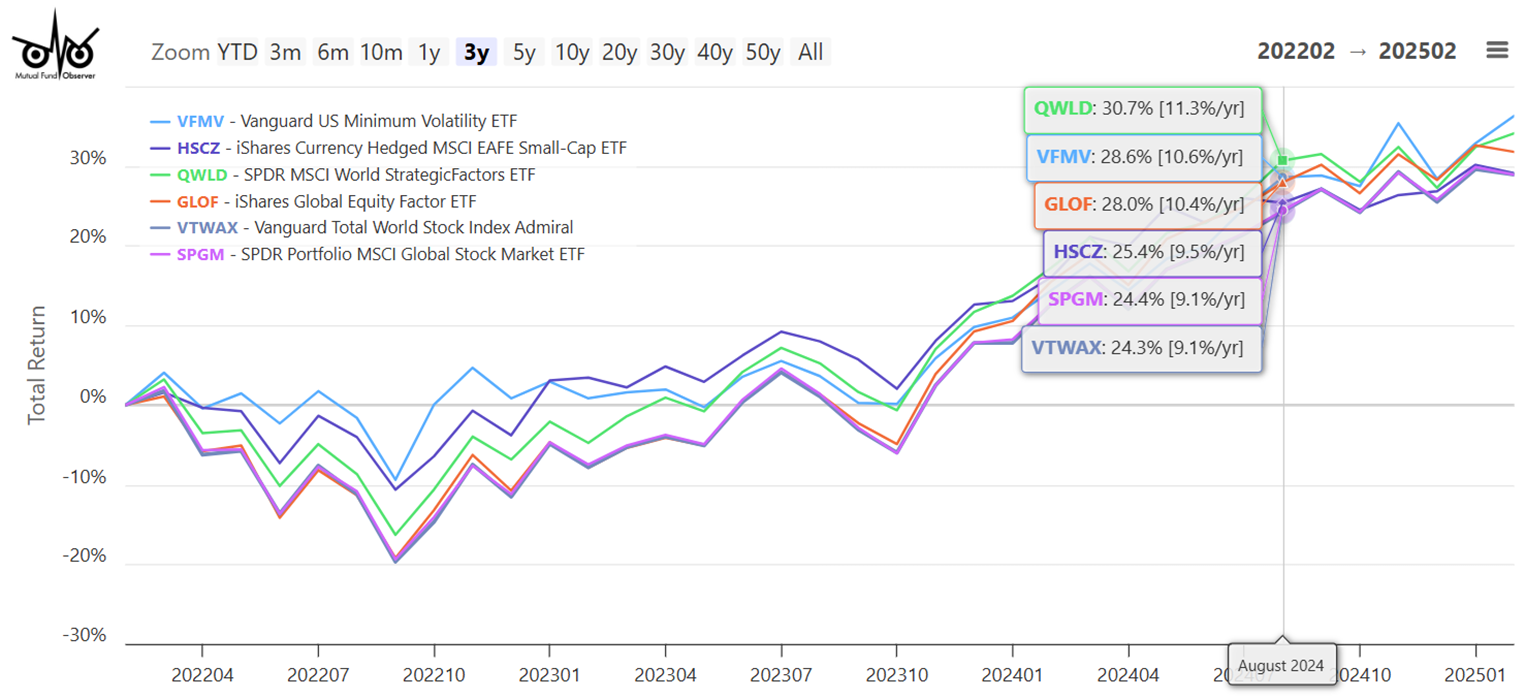

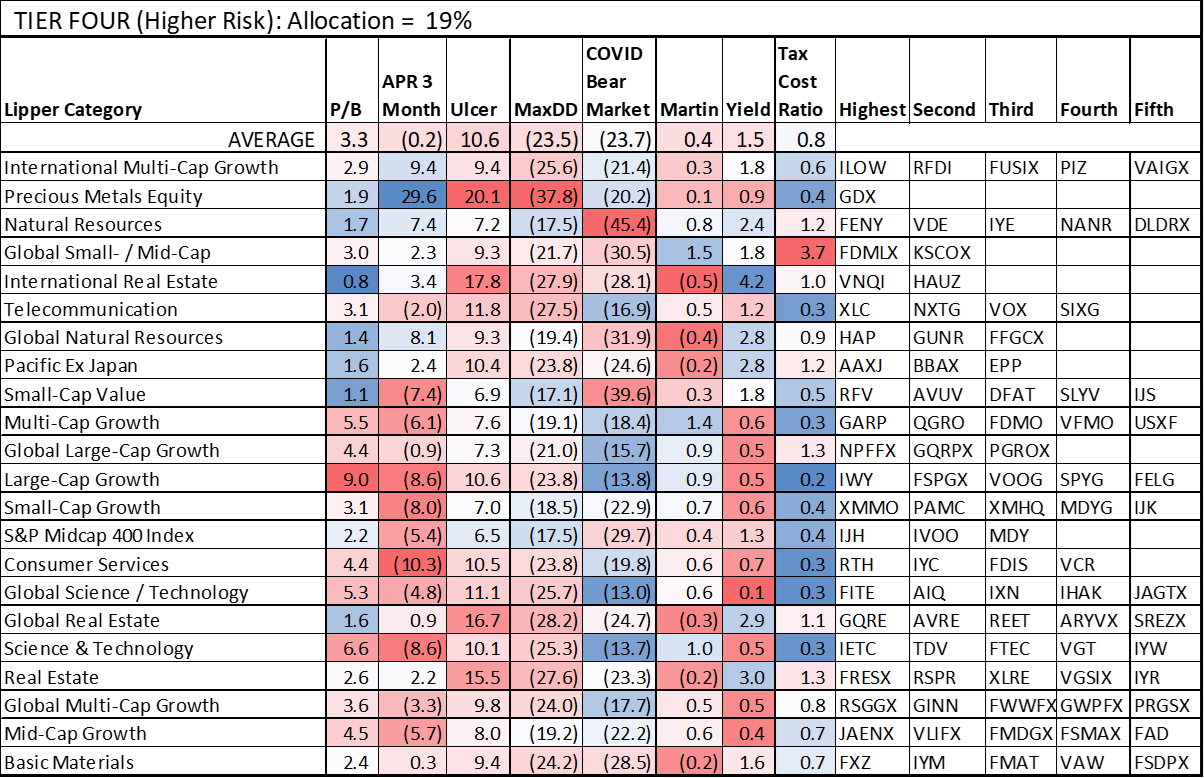

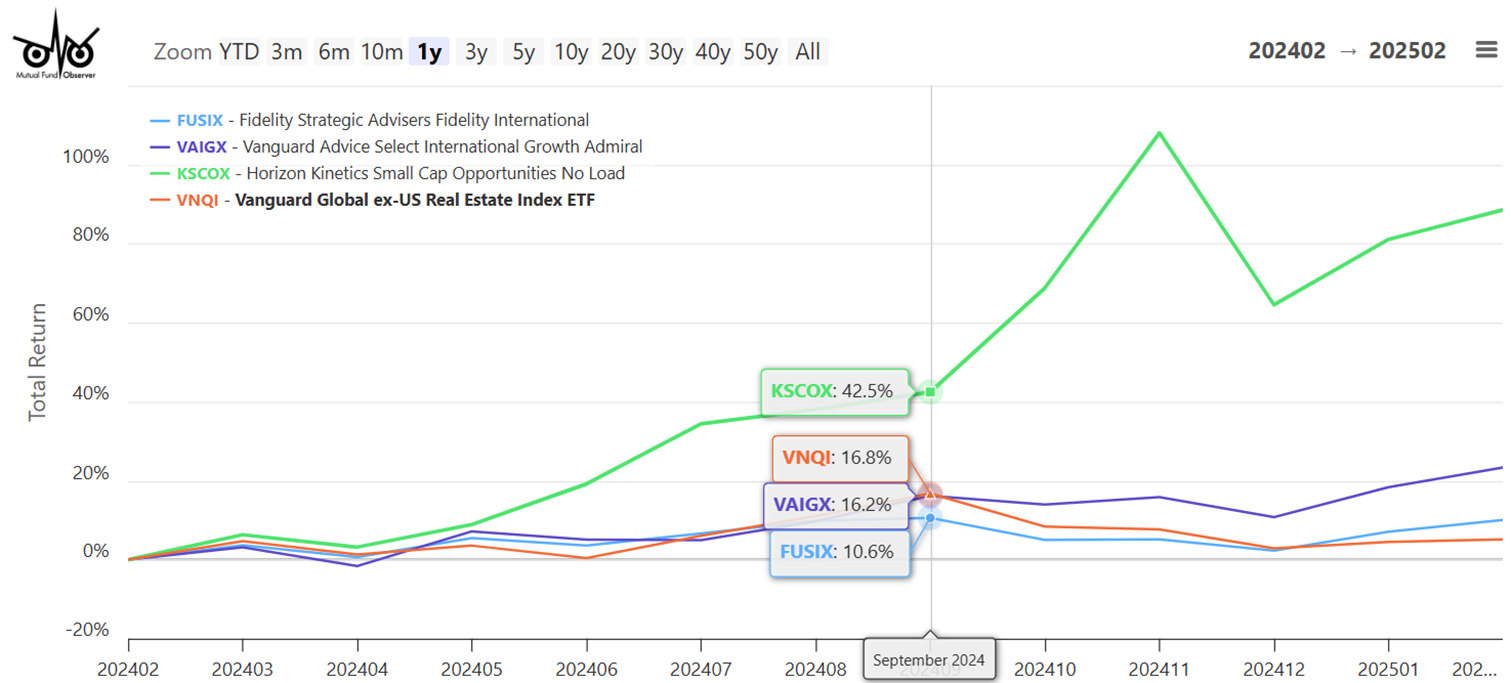

He follows that up with Equity Fund Ratings, where Bolin presents his four-tier system for evaluating equity funds based on risk, valuations, performance, and momentum. Each tier represents different risk-yield profiles, from Tier One (lower risk, lower valuations, higher yield) to Tier Four (higher risk). He highlights specific funds within each category, noting that international stocks are currently performing well while technology stocks have declined.

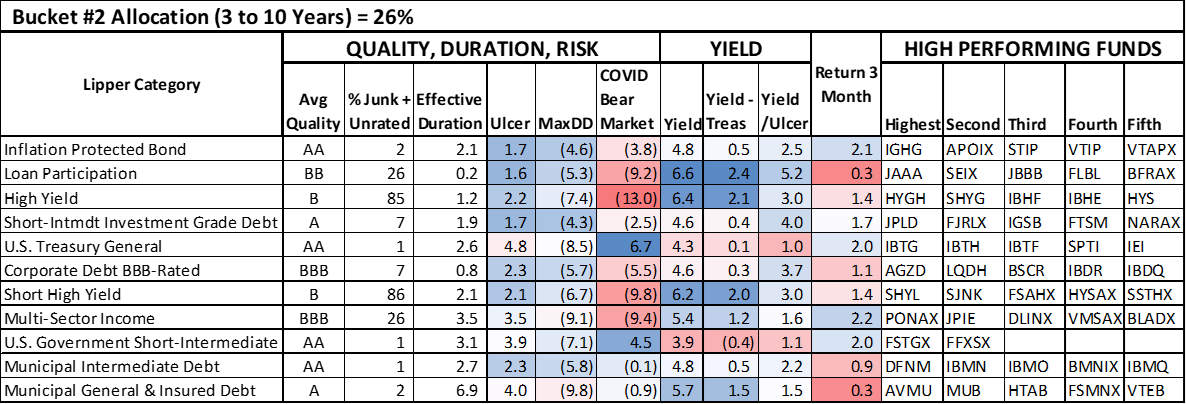

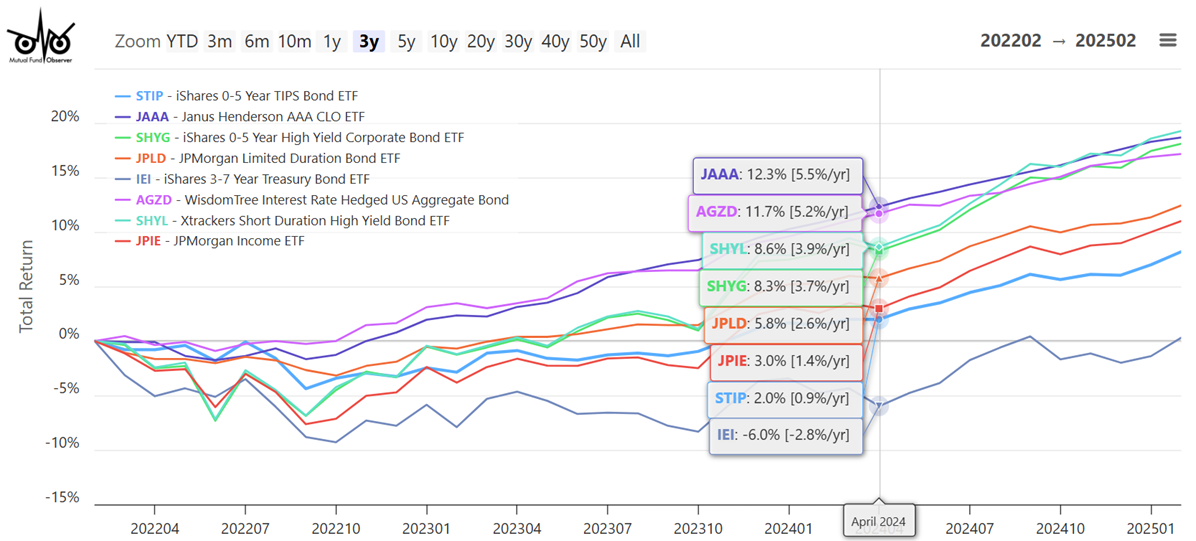

Lynn’s last article continues his inquiry into bonds and fixed-income as a competitor to equities. Investment Buckets for Bonds outlines Lynn’s bucket strategy for bond investments: Bucket #1 (safety, 1-3 years), Bucket #2 (intermediate, 3-10 years), and Bucket #3 (long-term, 10+ years). For each bucket, he evaluates bond categories and specific funds based on duration risk, quality risk, yield, and momentum, sharing his current allocations and recent performance data.

The Shadow, faithful as ever, offers a Briefly Noted take on the industry and its churning. Highlights include kudos to CrossingBridge, structural changes at two Schwab funds that might signal a broader judgment about where assets are going, and, driven by reader interest, the addition of a new feature: Launches and Conversions to help deal with the increasing pace of active fund to ETF conversions.

Winning strategies aren’t what you’d expect

If we were to ask what worked best over the past quarter-century, a generation of young investors (and many increasingly dotty senior investors) would say the same thing: tech works! Large works, growth works! Disruptors ruuuule!

Yeah, about that … not so much.

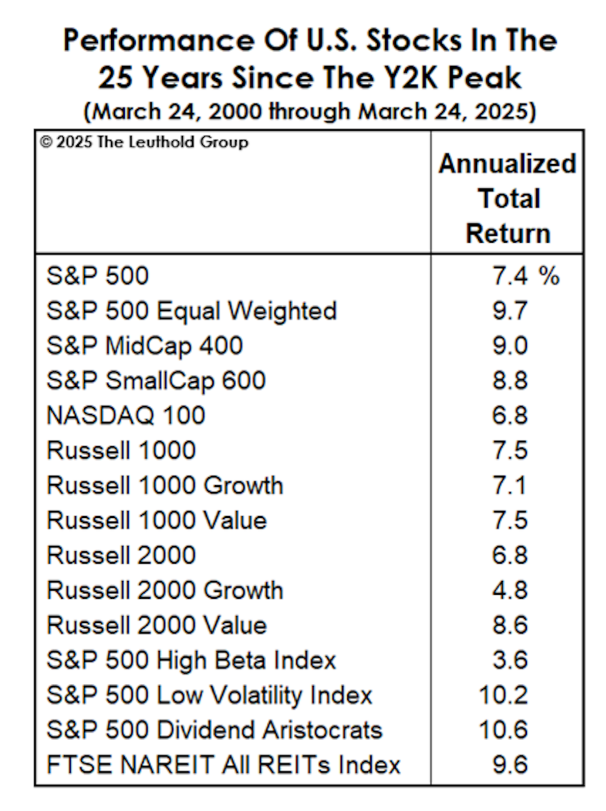

The good folks at Leuthold shared the data on precisely this question. If you bought into the market a quarter century ago, where should you have been? The answer is below:

Source: Leuthold Group, March 2025

Source: Leuthold Group, March 2025

Here’s the story:

Value beat growth, either by a little or by a lot, depending on the slice of the market.

Boring (low volatility, high dividends) beat exciting (high beta) by about 3:1.

Contrarian (the equal-weight 500) beat momentum (the 500) by over 200 bps per year.

Everything between tech and telecom.

Emerging beat developed international markets (by about 2.5% per year), though the US handily beat both.

“American exceptionalism” is the story that the US can count on being #1 – in influence, trade, tech, and market performance – because we’re special. More rational, more reliable, more resilient, more sensible, more pragmatic … less impulsive (looking at you, Italy!), less authoritarian, less erratic, less self-destructive, less xenophobic. If our actions undercut the judgments that others make of us, we should not be surprised when our exceptional performance evaporates.

Performance Update on a Chaos-Resistant Portfolio

In Building a Chaos-Resistant Portfolio, we noted that things were likely to be chaotic for rather longer than you’d like and offered suggestions for managing it. The theme of “chaos” is echoed by an increasing number of first-tier managers.

Trade policy inconsistencies, waning consumer confidence, and renewed recessionary concerns are all weighing heavily on broad market indexes. (J Dale Harvey, Poplar Forest Quarterly Letter, 4/2025).

The tariffs that the U.S. is imposing on its trading partners will bring about several costs that are important for investors to understand. Some of those costs are inherent to what a tariff is, while others stem from the fact that U.S. industrial policy has, and looks to continue to have, a huge amount of uncertainty associated with it. That continuing uncertainty will hit investment levels, return on capital and overall growth globally, with the U.S. bearing the brunt of it. (Ben Inker and John Pease, “Tariffs: Making the U.S. Exceptional, but Not in a Good Way,” GMO Quarterly Letter, 4/2025)

One set of suggestions might be translated as “get a life,” which is to say, stop doom-scrolling and attempting to micro-manage your portfolio. The other set of suggestions were to rely on good tacticians to worry on your behalf (FPA, Leuthold, and Standpoint), to increase your exposure to quality stocks (GQG), and to consider adding a short- or ultra-short fixed income fund into the mix. Here’s the performance of the eight funds we highlighted, YTD through the end of March 2025. “Great Owl” funds are flagged with a blue box.

| YTD, through 3/28/25 | ||

| Vanguard Total Stock Market | VTSMX | -4.85 |

| Quality | ||

| GQG Partners US Quality Value | GQHIX | 9.27 |

| GQG Partners US Select Quality Equity | GQEIX | -0.67 |

| GMO US Quality ETF | QLTY | -2.07 |

| Flexible | ||

| FPA Crescent | FPACX | -0.20 |

| Leuthold Core | LCORX | -0.8 |

| Standpoint Multi-Asset | BLNDX | -4.5 |

| Short-Term Fixed Income | ||

| Intrepid Income | ICMUX | 1.24 |

| RiverPark Short Term High Yield | RPHYX | 0.99 |

Source: Morningstar.com

The goal here is not to win in the short term. It’s to create a fund pairing (FPA and RiverPark, in my case) that is unusually resistant to downturns and driven by tested strategies.

ETF filings, from the ridiculous to the sublime

Tuttle Capital has filed for the UFO Disclosure AI Powered ETF (UFOD), which aims to invest in companies believed to have potential exposure to “reverse-engineered alien technology” based on government disclosures about UFOs. The ETF will allocate at least 80% of its assets to aerospace and defense contractors rumored to work on classified technology related to UFO research. Additionally, the ETF will short companies that could become obsolete due to any advanced alien technology that might be disclosed. The launch of UFOD is contingent on sufficient government disclosures about UFOs, and it is pending regulatory approval.

(sigh)

GQG has filed for the GQG US Equity ETF (QGUS), slated for launch in June 2026. The fund will be the GQG Partners US Select Equity strategy in an ETF wrapper. The fund has, predictably, clubbed its peers since its inception, averaging 11.7% per year compared to its peers’ 7.9%. A major distinction is that the ETF will charge 0.45%, while the fund charges 0.67%. In our assessment, the fund is cheap at that price, and the ETF will be a major bargain.

The GQG fund will be managed by a team managed by CIO/founder Rajiv Jain. As we noted in our profile of GQG Global Quality Dividend (5/2024):

If you believe that you need to invest against the prospect that markets are going to be marked by persistent if not crippling inflation, significant interest rates, and inconsistent growth, you should probably invest in high-quality stocks with sustainably high-dividend income. You’ll earn higher total returns over time, suffer less volatility, and enjoy an actual cash stream from your portfolio.

If that prospect intrigues you, no one has done it better for longer than GQG. They warrant your attention.

Credit to Eva Thomas of CityWire for catching the GQG filing (“GQG preps to enter ETF market,” 4/1/2025)

A Chasm of Need: How to Help in the Wake of USAID Defunding

A long-time member of the Observer community, who has rather more direct experience with such things than I, shared the following reflection on the federal government’s precipitous retreat from international engagement. Such aid programs have typically flowed from two distinct impulses:

- To strengthen America’s security by reducing the prevalence of pandemic diseases elsewhere (which would eventually reach here), to reduce the prevalence of political and economic instability elsewhere (which would eventually cost us more through military conflict or market losses), and to increase the US standing in the world (so-called “soft power diplomacy”) and

- To enact our shared sense of commitment to and compassion for our brothers and sisters in humanity.

Politicians have often fostered the myth of “massive giveaways” (rather, under 1% of the federal budget, and falling) and “welfare,” but those aren’t analytic statements. They’re political posturing. Until this year, they were mostly malignant noise. What follows is a friend’s report on the transition from one form of malignity to another and how we might make a difference as individuals even as our collective will falters.

On Friday, March 28, 2025, the U.S. Agency for International Development was officially shuttered, with only 15 statutorily required positions retained out of 10,000, and the remaining skeletal staff losing their jobs later this year. According to a Pew Research Center report from February 6, 2025, the U.S. was on track to deliver about $58 billion in international aid in FY 2025. That figure is a tiny percentage of the US federal budget but responsible for an enormous impact worldwide. The ripple effects from the defunding of the bulk of grants and contracts overseen by USAID are likely to be enormous. The loss of skills and processes developed to put together complex NGO funding networks adds another dimension to the problem.

On Friday, March 28, 2025, the U.S. Agency for International Development was officially shuttered, with only 15 statutorily required positions retained out of 10,000, and the remaining skeletal staff losing their jobs later this year. According to a Pew Research Center report from February 6, 2025, the U.S. was on track to deliver about $58 billion in international aid in FY 2025. That figure is a tiny percentage of the US federal budget but responsible for an enormous impact worldwide. The ripple effects from the defunding of the bulk of grants and contracts overseen by USAID are likely to be enormous. The loss of skills and processes developed to put together complex NGO funding networks adds another dimension to the problem.

U.S. citizens are not spared the effects of the defunding of USAID aid programs. According to AP reporting, “the vast majority of U.S. foreign assistance actually went through U.S.-based organizations.” Those organizations are going dark, and American workers are losing jobs.

U.S. citizens are not spared the effects of the defunding of USAID aid programs. According to AP reporting, “the vast majority of U.S. foreign assistance actually went through U.S.-based organizations.” Those organizations are going dark, and American workers are losing jobs.

The AP article (February 26, 2025) lists several nonprofits that have dedicated funding to groups affected by the loss of USAID program money. Unlock Aid, which advocated for USAID interests, has set up the Foreign Aid Bridge Fund to support frontline groups working to deliver medicines, immunizations, nutrition, loans for small businesses, and other life- and livelihood-saving interventions.

Because of the complex structure of donor organizations, getting aid as directly as possible to those in need is something of a conundrum. For now, interested parties might also consider the UN World Food Program, which received about half its funding from USAID and has now closed its southern Africa office.

Thanks, as ever . . .

To our faithful “subscribers,” Wilson, S&F Investment Advisors, Greg, William, William, Stephen, Brian, David, and Doug, thanks! We wave, with special delight, to our newest “subscriber,” Altaf from Naperville.

To Tom & Mes from Tennessee (we totally had to search for your hometown and discovered … the best coffee shop trailer in Tennessee?) and to John from PA, thanks! And for more than just financial support. You make a difference.

It’s planting time. We’re waiting for our garlic bulbs to arrive, likely late this month, but I’ve already been pulled out winter grasses, turning the compost pile and scattering wildflower seeds.

Planting is an act of hope. Gardening is a gesture of resilience. Pursue both, dear friends.

As ever,